Carmen Reinhardt reflects on the economic cycle and expectations for inflation in the coming months.

Until the global financial crisis of 2008-2009, deflation had all but disappeared as a concern for policymakers and investors in the advanced economies apart from Japan, which has been subject to persistent downward pressure on prices for nearly a generation. And now deflationary fears are on the wane again.

By the mid-1960s, the advanced economies began an era of rising inflationary pressures, ignited largely by expansionary fiscal and monetary policies in the United States, and acutely compounded by the oil price hikes of the 1970s. Stagflation, the combination of low economic growth and high inflation, became a buzzword by the end of that decade.

Most contemporary market forecasts extrapolated those trends, predicting an uninterrupted upward march in oil and commodity prices. Inflation came to be seen as chronic, and politicians looked toward price controls and income policies. Real (inflation-adjusted) short-term interest rates were consistently negative in most of the advanced economies.

FROM STAGFLATION TO DISINFLATION

Carmen Reinhart

Federal Reserve chairman Paul Volcker’s monumental tightening of US monetary policy in October 1979 ended that long cycle.

Sustained dollar appreciation should limit price gains for a broad range of imported goods and their domestic competitors

Stagflation gave way to a new buzzword: disinflation, which accurately characterised many advanced economies, as inflation rates fell from double digits.

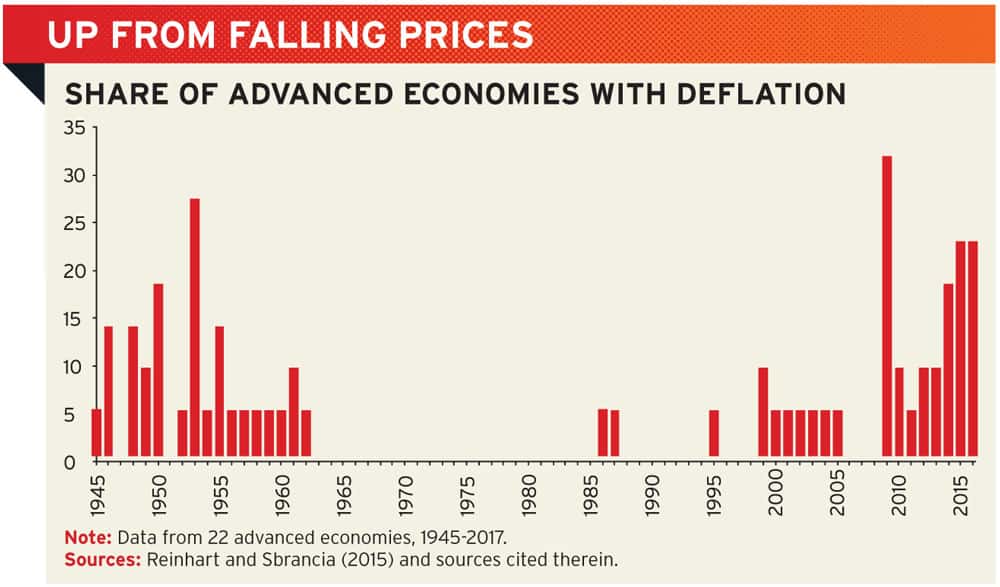

But disinflation is not the same as deflation. As shown in the figure, between 1962 and 1986 not a single advanced economy recorded an annual decline in prices.

In many emerging markets inflation rates soared into triple digits, with several cases of hyperinflation. As late as 1991, Greece had an inflation rate of about 20%. Even in historically price-stable Switzerland at that time, inflation was running above 5%.

BATTLING DEFLATIONARY FORCES

This seems a distant memory after the steady decline in prices in Greece since 2013, alongside a debt crisis and collapse in output. The Swiss National Bank, for its part, has been battling with the deflationary effects of the franc’s dramatic appreciation over the past few years.

The deflationary forces were unleashed by the major economic and financial dislocations associated with the deep and protracted global crisis that erupted in 2008. Private deleveraging became a steady headwind to central bank efforts to reflate.

In 2009, about one-third of advanced economies recorded a decline in prices – a post-war high. In the years that followed, the incidence of deflation remained high by post-war standards, and most central banks persistently undershot their extremely modest inflation objectives (around 2%).

TURNING POINT

Because US President Donald Trump’s stimulus plans are procyclical – they are likely to gain traction when the US economy is at or near full-employment – they have reawakened expectations that the US inflation rate is headed higher. Indeed, inflation is widely expected to surpass the Federal Reserve’s 2% objective.

But tighter monetary conditions act to mitigate the magnitude of the inflation spurt: while the expected rise in US policy rates is the most modest and gradual ‘normalisation’ in the Fed’s history, sustained dollar appreciation should limit price gains for a broad range of imported goods and their domestic competitors.

CENTRAL BANK TOLERANCE

This expected turning point in the behavior of prices is not unique to the US. If the International Monetary Fund’s projections for 2017 are approximately correct, this year will be the first in a decade that no advanced economy is experiencing deflation.

Perhaps the long-awaited effects of the historic monetary expansion are finally yielding fruit. Most likely, currency depreciation in the UK, Japan and the eurozone has been a catalyst.

If 2017 really does mark a broad reversal of a decade of deflation, it is reasonable to expect that most major central banks will not be inclined to overreact if, after a decade or so (longer for Japan) of mostly downside disappointments, inflation overshoots its target.

Furthermore, the view that higher inflation targets (perhaps 4%) may be desirable (because they would provide central banks with more space to lower interest rates in the advent of a future recession) has gained ground in some academic and policy quarters.

Of course, there may be yet another factor motivating major central banks’ tolerance for higher inflation. But their leaders may be unwilling to acknowledge it openly: as I have argued elsewhere, a steady dose of even moderate inflation will help to erode the mountains of public and private debt that advanced economies have built up in the past 15 years or so.