US equities surged to record its best week since December 2011 as US tech stocks were seen as been the key drivers of this life, writes Ian Slattery.

Ian Slattery

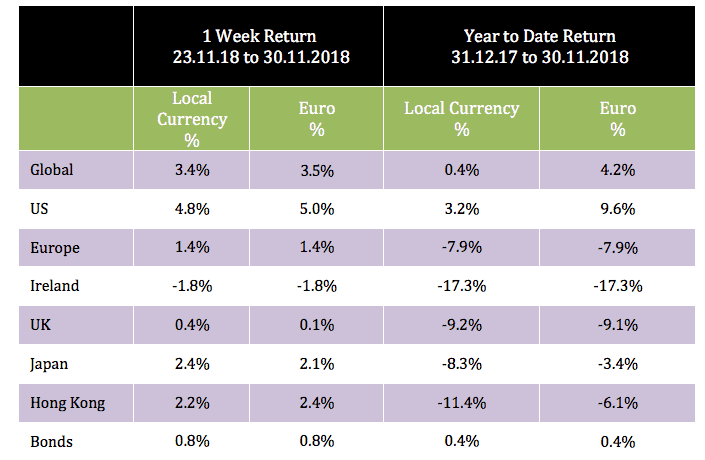

Global equities advanced, with U.S. equities recording their best weekly gain since December 2011. In a reversal from the past month, higher-valuation growth shares outperformed, with the health care and technology sectors notably strong.

Trade headlines had threatened to take centre stage but instead, it was Fed Chairman Jerome Powell. His dovish comments leading investors to conclude that rate hikes might not be as aggressive in 2019 as first thought.

Economic data was mixed during the week. Home sales dropping almost 9% with pending home sales and home prices also weaker than expected. On a positive note, both personal spending and income rose at a steady pace in October.

The global equity index advanced 3.4%, erasing last week’s decline. Large cap US tech stocks were the primary drivers.

Oil prices remained under pressure, finishing the week at $50.93 /barrel, although the price did rally over the weekend as OPEC outlined that supply cuts are in the pipeline. Gold ended the week relatively unchanged at $1,223 per troy ounce, while Copper declined to $6,227 per metric tonne.

The weaker-than-expected economic data pushed the yield on the 10-year bond to 2.99%. The German equivalent also moved lower to 0.31%.

The EUR/USD rate ended the week at 1.132, with the EUR/GBP at 0.887

THE WEEK AHEAD

Monday 3rd December:

Last month’s PMI Manufacturing in Europe was 52.0. The expectation for this month is 51.5 and 51.6 in Germany. The consensus range in the US is 55.2 to 55.4, while the ISM manufacturing index in the U.S. is forecast between 56.0 and 58.3.

Wednesday 5th December:

Retail sales in Europe are forecast to increase 1.1% y-y. The expectation for the PMI Composite is 52.4, below the prior reading of 53.1. The Beige Book, used at FOMC meetings where the Fed sets interest rate policy, is also released today.

Thursday 6th December:

The consensus is for initial jobless claims in the US to fall to 225k, from the prior reading of 234k. The US International Trade deficit is expected between $52.7 to 55.4 billion. Factory orders are forecast to decline 2% m-m, from the prior reading of 0.7%.

The team at Zurich Investments is a long established and highly experienced team of investment managers who manage approximately €23.5bn in investments of which pension assets amount to €10.8bn. Find out more about Zurich Life’s funds and investments here.

w: zurichlife.ie/funds t: @ZurichLife

l: linkedin.com/company/zurich-life-assurance-plc