There was a robust start to the year for the investment markets with record highs for equities, writes Ian Slattery.

Ian Slattery

The Dow, S&P 500, and NASDAQ all hit record highs last week, with the Dow crossing 25,000 points for the first time ever on Thursday as the impact of higher economic growth and US tax cuts continue to be digested.

December payroll data for the US disappointed, with 148,000 jobs created versus an expectation of 193,000. The underwhelming data was attributed to lower-than-expected retail jobs over the festive period, as online sales continue to take a grip on the market.

The odds of another US rate rise in March currently stands at close to 80%, from just 10% four months ago.

However, markets took the miss in their stride as participants remain positive on the economy. The odds of another US rate rise in March currently stands at close to 80%, from just 10% four months ago. US ten-year yields rose (yields move inversely to price) as the demand for lower risk assets declined throughout the week.

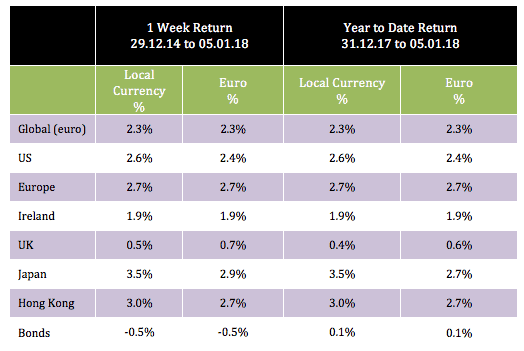

The global index in euro terms was up a solid 2.3% last week, in what was a strong start to the year. Japan led the way, up nearly 3% in euro terms. Oil continued its recent strength with another positive week, and is now above the $60/barrel mark. Copper closed down just over 2% for the week whilst gold was up 1.25%.

The ten-year US bond yield finished the week at 2.48% as interest rate expectations ticket up. The ten-year German equivalent was at 0.44% from 0.42%. And the EUR/USD rate closed the period at 1.20, while EUR/GBP was at 0.89.

THE WEEK AHEAD

Tuesday 9 January

Eurozone unemployment data for November is released, where the rate is expected to tick up slightly to 8.9% from 8.8%.

Thursday 11 January

The minutes from the latest ECB meeting are released. No changes to the current policy are envisaged but the text is always closely watched for indications of future policy.

Friday 12 January

US retail sales data for December goes to print where the consensus estimates a growth rate of 0.4% (month-on-month). Inflation data is also released, where a monthly increase of 0.1% is forecast.

The team at Zurich Investments is a long-established and highly-experienced team of investment managers who manage approximately €21.9bn in investment of which pension assets amount to €9.9bn. To find out more about Zurich Life’s funds and investments, w: zurichlife.ie/funds t: @ZurichLife

l: linkedin.com/company/zurich-life-assurance-plc