China’s government is attempting a balancing act that even Beijing may not pull off, writes Mark Godfrey as he notes that the country’s juggling act gets harder to balance.

While trying to cope with slower economic growth, the Chinese government is seeking to make the RMB an international currency through a trading link-up between the Hong Kong and Shanghai stock markets and arranging government-to-government currency swaps (thus theoretically allowing RMB to flow outside of China) even as they also seek to limit outflows of private funds – especially ill-gotten funds – and collect more taxes from the super-rich.

But while the boom years of recent decades created fortunes in real estate and manufacturing, it’s apparent that some of country’s elite are losing confidence in the economy and the system that drives it. And thus the scramble to get money out of the country has picked up pace.

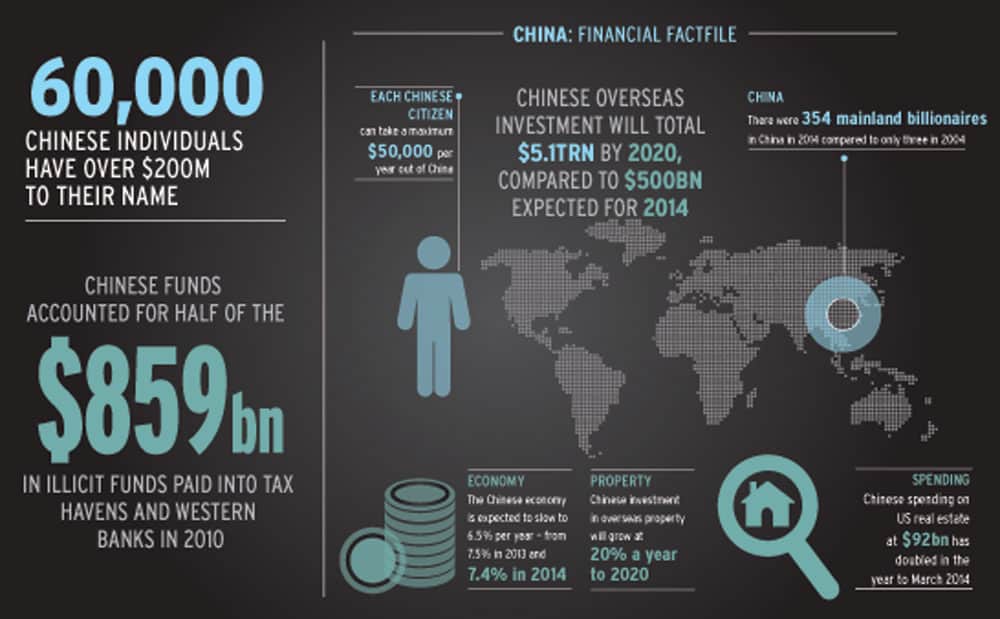

Anyone with time to wander the aisles at the recent China Luxury expo in Beijing would have, among waif-like models (adorning sports cars and yachts) and cigar salesmen have encountered booths for ‘immigration consultants’ and California realtors. They were all there to target China’s wealthy, the tu hao (‘tacky rich’ in Mandarin) as the nouveau riche have become known in local colloquial terms. There are 354 mainland billionaires in 2014 compare to only three in 2004 according to Hurun, a consultancy and magazine following China’s rich, which estimates 60,000 Chinese individuals have over $200m to their name.

The uber-wealthy are the targets of a Chinese salesman for a European yacht maker who explained to this writer at the Beijing luxury fair that its $45m yachts are tailor made to the tastes of Chinese tu hao, with ‘baths designed to fit a man and his mistresses’.

Showing off comes easy to China’s new rich but in many cases China’s big spenders may however have been reverting to big ticket purchases as a way of getting money out of the country. A source at a leading bank in wealthy Guangdong province explained how a favourite ploy is to purchase antiques and artwork overseas at often vastly inflated prices through a middleman who takes a cut before banking the money in a bank account overseas for the original Chinese buyer.

The new rich may prove a kind of canary in a coal mine, and the eagerness to get their money out suggests a lack of confidence in government reform delivering further economic growth.Chinese businesses are likely to remain keen to shift money overseas as the economy here will likely slow to 6.5% per year (from 7.5% in 2013 and 7.4% in 2014) under projections of the 13th Five Year Plan set to run from 2016-2020. Government is buying time for structural reforms but it could lead to a sharper fall-back and then the exit of funds will increase.

Share highs and lows

Even though government initiatives managed to drive the Shanghai A-shares index to new highs in late 2015, Chinese money continues to make for the exit.

The scale of China’s funds and the enthusiasm to get funds out of China and into higher yield assets overseas was hinted at in the acquisition by Gingko Tree Investment, ironically a unit of the body charged with overseeing forex controls, the State Administration of Foreign Exchange (SAFE), of a 70,000 sqm office complex in Brussels in December. Gingko Tree, which serves as the investment arm of China’s, joined German fund manager Hannover Leasing in the $319 million purchase, the latest in a flurry of investments by Chinese government investment funds in western real estate.

Chinese spending on US real estate at $92bn has doubled in the year to March 2014, making China, according to the US National Association of Realtors, the number one spender on American real estate. Given mass tax evasion and limits on personal forex transactions (each Chinese citizen can take a maximum $50,000 per year out of China) it’s not surprising that Chinese funds accounted for half of the $859bn in illicit funds into tax havens and western banks in 2010, according to the Global Financial Integrity, an advocacy group.

Overseas investments

There is a case for seeing the expansion of China’s economy as a natural trigger for legitimate overseas investment and thus shifting of funds abroad. Chinese overseas investment will total $5.1trn by 2020, compared to $500bn expected for 2014, according to the IMF. That would amount to 27% of China’s GDP.

However, if all Chinese are legitimately allowed to convert their money the sums involved in the scenario of a convertible RMB are truly huge. A ‘hasty’ opening of the capital account would see $1.35trn flowing out in an opening up process, warns the frequently contrarian (and correct) independent economist Andy Xie in Beijing.

“Ultimately you’re seeing $2.25trn being shifted overseas compared to $900bn coming in from FDI, which would be 15% of GDP,” notes Xie. He bases the figures on the experience of Japan which saw 10% of its GDP exit when it fully liberalised the Yen in 1980.

Enticing incentives

Another potential trigger of funds going overseas – a new property registration system is coming into operation in March 2015. It’s seen as a way of ferreting out officials who own large real estate portfolios, often by proxy. Thus, there’s an increased incentive to invest abroad. Chinese investment in overseas property will grow at 20% a year to 2020, predicts property consultancy Savills.

Chinese financial institutions have also been ramping up their overseas investments, doubling their real estate investments year on year in 2013 to $13.5bn. China’s commerce ministry puts overseas direct investment into the US in 2013 at $10bn ($6bn was spent in the EU) while the Rhodium Group puts the total of Chinese investment into North America in 2013 at $14bn.

Interest rates

The full liberalisation of China’s currency controls will depend on how successful China is in liberalising the interest rates and how this is sequenced with liberalisation of foreign exchange controls but also on reforms restructuring the Chinese economy going right. If some Beijing planners have their way the RMB, not the dollar, may soon be in everyone’s pockets. But for now the tu hao are figuring out how to navigate currency controls and get money out.