Sterling saw its biggest one-day gain against the dollar since 2008, up 2.9%, in the immediate aftermath of UK prime minister Teresa May’s speech last Tuesday. Ian Slattery reports.

The markets struggled to find direction in the week leading up to the inauguration of Donald Trump, and some of the uncertainty over his future policies began to leak into financial markets.

Ian Slattery

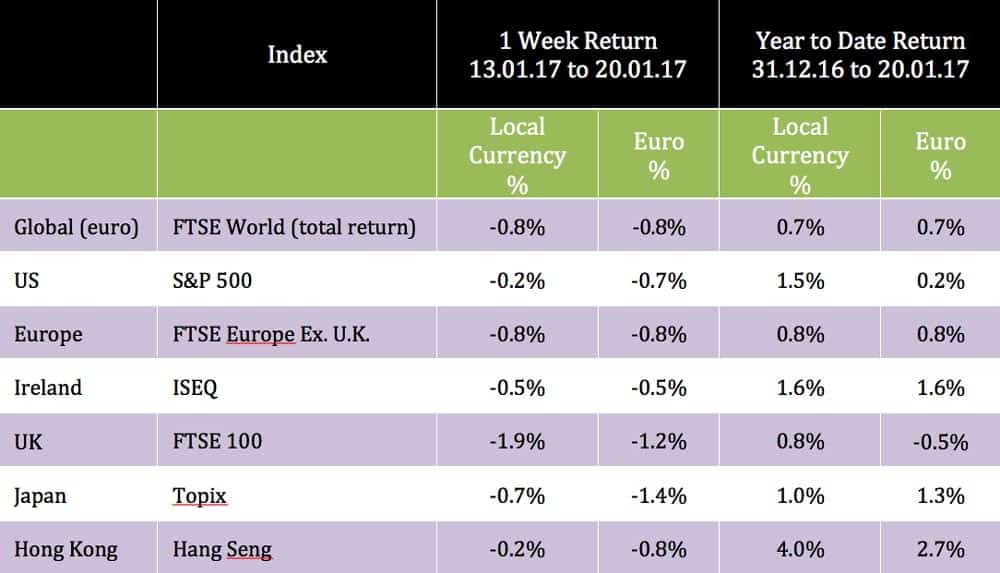

The S&P 500 index closed with a small decline, and has essentially been trading sideways since mid-December.

US Treasuries saw prices fall during the course of the week as a more ‘hawkish’ stance from the Fed, coupled with stronger economic data, drove yields higher.

UK Prime Minister Teresa May provided some clarity in her speech last Tuesday, and markets are now expecting a ‘hard Brexit’ from the EU. Sterling saw its biggest one-day gain against the dollar since 2008, up 2.9%, in the immediate aftermath of the speech.

The UK Supreme Court is expected to rule this week on whether parliamentary approval is required to trigger Article 50, but irrespective of their decision markets still forecast the move by the end of March.

The global index fell 0.8% over the course of the week, as modest economic data was offset by US policy uncertainty concerns.

The global index fell 0.8% over the course of the week, as modest economic data was offset by US policy uncertainty concerns.

Gold saw another weekly price gain, as investors perhaps utilise it as an inflation hedge

Copper fell over the course of the week, down 2.4% in dollar terms. Gold saw another weekly price gain, as investors perhaps utilise it as an inflation hedge.

The US 10-year bond yield saw a volatile week, falling to 2.33% before finishing at 2.47%, from 2.40% a week ago. The yield on the equivalent German Bund also rose, closing the week at 0.42%, from 0.34%.

The euro was up once again against the dollar over the week, with the EUR/USD rate closing at 1.07.

THE WEEK AHEAD

Tuesday January 24th

Eurozone manufacturing and services PMIs (purchasing managers’ index) are released. Considered a strong gauge of economic activity they will be closely watched for continuing signs of improvement. The consensus is for a manufacturing reading of 54.8, with the services expected at 53.9. A reading in either above 50 signifies an expansion in activity.

Thursday January 26th

A preliminary reading for UK Q4 GDP goes to print where growth of 0.5% (quarter-on-quarter) is envisaged. The Q3 growth figure has been previously confirmed at 0.6%.

Friday January 27th

In the US all eyes will be on the advance release of Q4 GDP. The consensus is for a growth figure of 2.0%, down from 2.2% reading from Q3.

The team at Zurich Investments is a long established and highly experienced team of investment managers who manage approximately €20.8bn in investment of which pension assets amount to €9.9bn. To find out more about Zurich Life’s funds and investments, w: zurichlife.ie/funds, Twitter: @ZurichLife, LinkedIn: linkedin.com/company/zurich-life-assurance-plc